Promotions: legal and tax issues

On 4 October 2014 PwC’s Academy held its October session – in the spectacular Eiffel Palace building on Bajcsy-Zsilinszky Road – where promotion-related legal and tax issues were discussed.

Dr Judit Firniksz, lawyer and legal expert of Réti, Antall and Co. PwC Legal was the first speaker. She gave the legal definition of promotion and talked about the responsibility and liability of those participating in organising a promotion, and also talked about the types of advantages consumers can enjoy. Then she listed traps which are characteristic of promotions. The first four traps can occur in communicating the promotion – consumers must be informed in detail about everything, for instance the promotional price must be indicated in a fashion that it is easily comparable with the normal price. The next three traps have to be avoided when organising prize games; in this domain organisers must pay special attention to trademarks, logos and game concepts, with special regard to online solutions and mobile apps. Dr József Németh, lawyer and legal expert of Réti, Antall and Co. PwC Legal introduced two more traps from the field of data protection and management. Both experts listed several examples to illustrate the traps, from the football World Cup to online games. Péter Honyek, senior manager and tax expert of PwC talked about promotions, benefits and prize games from a taxation perspective. He touched upon personal income tax matters in connection with various prize games and draws, for instance it turned out that the formal framework used for prize games and draws decides whether something won is subject to a tax or not – both the organiser and the consumer side was analysed in this respect. Instead of the ‘lottery’ form it is better to use a prize draw framework or a quiz/competition format. Prize draws may entail complicated administrative work but they guarantee perfect safety. Practically all popular prize types can be drawn – car, fridge, trip – with the exception of cash. 119 percent of the prize’s value forms the tax basis and the tax is 16 percent: altogether there is a 19.04-percent tax burden on the prize, which has to be paid by the organiser. Quizzes and competitions where the prize isn’t money require less administrative work, and the tax burden is 19.04 percent in this case as well. Business and promotional gifts can be given without having to pay taxes if they are directly connected to purchasing. The discount is allowed to be bigger than the value of the product/service purchased. Product samples can be distributed free of any personal income tax and VAT payment obligation. However, samples aren’t allowed to have the capacity to be used in the long term or to achieve other goals. Szabolcs Varga, VAT expert of PwC first grouped discounts according to the time of offering them and then based on the type of performance. He used the Elida Gibbs case to illustrate the regulation on using money refund to reduce the tax basis, which is possible as of 1 January 2014. At the end of the event PwC experts were answering questions.

Dr Judit Firniksz, lawyer and legal expert of Réti, Antall and Co. PwC Legal was the first speaker. She gave the legal definition of promotion and talked about the responsibility and liability of those participating in organising a promotion, and also talked about the types of advantages consumers can enjoy. Then she listed traps which are characteristic of promotions. The first four traps can occur in communicating the promotion – consumers must be informed in detail about everything, for instance the promotional price must be indicated in a fashion that it is easily comparable with the normal price. The next three traps have to be avoided when organising prize games; in this domain organisers must pay special attention to trademarks, logos and game concepts, with special regard to online solutions and mobile apps. Dr József Németh, lawyer and legal expert of Réti, Antall and Co. PwC Legal introduced two more traps from the field of data protection and management. Both experts listed several examples to illustrate the traps, from the football World Cup to online games. Péter Honyek, senior manager and tax expert of PwC talked about promotions, benefits and prize games from a taxation perspective. He touched upon personal income tax matters in connection with various prize games and draws, for instance it turned out that the formal framework used for prize games and draws decides whether something won is subject to a tax or not – both the organiser and the consumer side was analysed in this respect. Instead of the ‘lottery’ form it is better to use a prize draw framework or a quiz/competition format. Prize draws may entail complicated administrative work but they guarantee perfect safety. Practically all popular prize types can be drawn – car, fridge, trip – with the exception of cash. 119 percent of the prize’s value forms the tax basis and the tax is 16 percent: altogether there is a 19.04-percent tax burden on the prize, which has to be paid by the organiser. Quizzes and competitions where the prize isn’t money require less administrative work, and the tax burden is 19.04 percent in this case as well. Business and promotional gifts can be given without having to pay taxes if they are directly connected to purchasing. The discount is allowed to be bigger than the value of the product/service purchased. Product samples can be distributed free of any personal income tax and VAT payment obligation. However, samples aren’t allowed to have the capacity to be used in the long term or to achieve other goals. Szabolcs Varga, VAT expert of PwC first grouped discounts according to the time of offering them and then based on the type of performance. He used the Elida Gibbs case to illustrate the regulation on using money refund to reduce the tax basis, which is possible as of 1 January 2014. At the end of the event PwC experts were answering questions.

Related news

Related news

Brake on Shein’s growth in Europe

🎧 Hallgasd a cikket: Lejátszás Szünet Folytatás Leállítás Nyelv: Auto…

Read more >

GKI: High base rate, low inflation?

🎧 Hallgasd a cikket: Lejátszás Szünet Folytatás Leállítás Nyelv: Auto…

Read more >

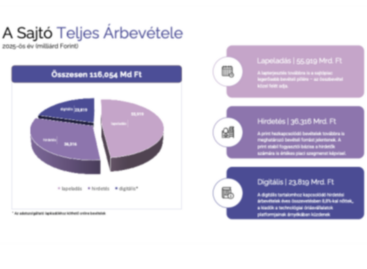

The domestic press market maintained its stability in 2025, although the expansion in real terms was minimal

🎧 Hallgasd a cikket: Lejátszás Szünet Folytatás Leállítás Nyelv: Auto…

Read more >

{kind=link}