Taxation quiz in Eastern Europe

The contradiction between national systems of taxation and the international business environment is pointed out in a recent report by PricewaterhouseCoopers about tax legislation in Eastern European countries. Taxes are fixed without regard to the international nature of business, which often leads to double taxation, contradictory obligations or the increase of the tax burden. It is not the tax rate which reveals the most about expected tax burden but rather the definition of the organisations subjected to a specific tax. Who or what might be exempted from tax ? Is there an agreement against double taxation in effect between the country of the investor and the country of the investment? What relations exist between the two systems of taxation? Investors should also have a detailed knowledge of the tax allowances and subsidies available, as there are a number of areas enjoying preferential status in all Eastern European countries, where even a nominally heavy tax burden may be offset by these. Since tax authorities intend to maximise tax revenues of their own countries, investors should also be familiar with the relationship between national tax legislation and international regulations and the possibilities for applying the provisions of international agreements.

Related news

Related news

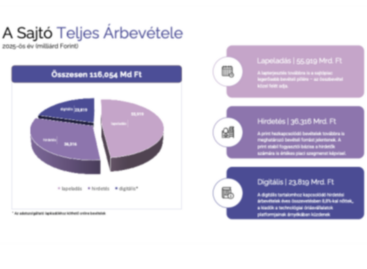

The domestic press market maintained its stability in 2025, although the expansion in real terms was minimal

🎧 Hallgasd a cikket: Lejátszás Szünet Folytatás Leállítás Nyelv: Auto…

Read more >

Hungarian Advertising Association: solid growth in 2025, but still lagging behind 2019

🎧 Hallgasd a cikket: Lejátszás Szünet Folytatás Leállítás Nyelv: Auto…

Read more >

Generation Z vs. senior executives: young people are ready, companies need to act now

🎧 Hallgasd a cikket: Lejátszás Szünet Folytatás Leállítás Nyelv: Auto…

Read more >

{kind=link}