Coface had its 15th Country Risk Conference, no change for Hungary

On the occasion of its 15th Country Risk Conference, Coface is expecting a moderate slowdown of the global economy. Among the risks to be monitored are the continued tension with the sovereign risks in the euro zone and the financing of growth in the emerging countries. Coface indicates that it is now the time of converging risks between the advanced countries and the emerging countries who have seen their rating improve with the test of the crisis.

If when country rating was launched in 2001, Coface was following 130 countries, it is now rating 156 countries of which 28 are so-called advanced countries.

In 2011, a key issue for the country risk will be private debt monitoring and growth financing.

According to Coface's forecasts, worldwide growth should slow down in 2011 at 3.4% compared to 4% in 2010, under the combined effects of debt reduction in the private sector, the setting up of restrictive budget policies in Europe, the possible rise in raw materials and the expected slowing in worldwide trade. The advanced countries will show growth of 1.8% compared to 2.3% in 2010 and the euro zone will experience limited growth deceleration (1.4% compared to 1.7% in 2010). This moderated drop will have a negative impact on the average credit risk for companies but the impact will be highly contained as the growth differential between 2010 and 2011 is limited to 0.6 point of GDP.

The big winners of the crisis are the emerging countries, which will continue the solid growth trajectory in 2011 with a slight slowdown: 6.2% compared to 6.7% in 2010. Contrary to the euro zone, where the private debt bubble has resulted in sovereign crises, activity in the emerging countries is not handicapped by the weight of private debt. However, the emerging countries are not immune to a surge in indebtedness in the private sector. Indeed, how should the investment boom that we shall still see in 2011 be financed? We therefore need to monitor two types of profiles:

Ø the “Polish-Brazilian” profile: companies have a tendency to go into debt abroad as the local banks are too reticent and the domestic rates are prohibiting, leading to the risk of having in these countries counterparties with more and more debt in foreign currency;

Ø the “Chinese-Vietnam” profile: companies increase their debt in local currency with domestic banks which are often not in a position to correctly analyse the risks. Entities with high debt and sometimes not very transparent could have difficulties.

A new phenomenon: the convergence between the risks in advanced countries and emerging countries is getting stronger

Based on its experience in evaluating country risks, Coface is observing a positive trend in terms of the number of changes in country ratings for the year 2010, discarding a “double dip” scenario. Although in 2009 Coface carried out 23 upgradings or putting under positive watch and 47 downgradings or putting under negative watch, in 2010 it reclassified or placed under positive watch 47 countries and downgraded or placed under negative watch only 6 countries.

The worldwide panorama of the country risk presented in the 2011 conference underlined a pronounced scissor effect for the risks between the advanced countries and the emerging countries linked to the stability of the performance of the latter and to the resistance of the payment experience observed by Coface with the companies from emerging economies during the crisis. The emerging countries have high and stable rates of activity and strong financial solidity while the risks are degraded for the advanced countries. Among the latter, only 9 out of 28 have returned to their pre-crisis level.

Before the crisis, the lowest rating in the advanced countries was A2; 9 emerging countries had ratings greater than or equal to A2. In 2010, the lowest rating in the advanced countries was A4. Twenty-seven emerging countries including China, Turkey, Brazil, India and Poland have ratings greater than or equal to A4 and now have a better ratings than Greece, Ireland and Portugal, subject to the debt bubbles whether private or public. Turkey is now only one notch below the United Kingdom and Poland has a better rating than Iceland.

“Traditionally the idea of country risk was reserved for emerging economies with a major risk linked to the foreign currency component of the debt of the emerging countries. However, the euro zone has demonstrated that it is possible to be in a crisis with very high external debt but in “local currency”. This working framework is falling apart”, explains François David, Chairman of Coface. “These changes confirm our choice of methodology: Coface has never really made a distinction in terms of nature between the emerging countries and the advanced countries”.

Related news

Related news

Brake on Shein’s growth in Europe

🎧 Hallgasd a cikket: Lejátszás Szünet Folytatás Leállítás Nyelv: Auto…

Read more >

GKI: High base rate, low inflation?

🎧 Hallgasd a cikket: Lejátszás Szünet Folytatás Leállítás Nyelv: Auto…

Read more >

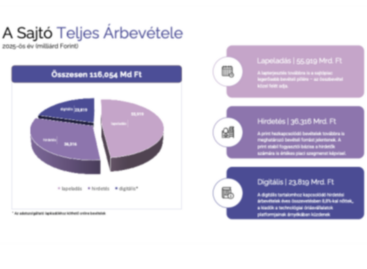

The domestic press market maintained its stability in 2025, although the expansion in real terms was minimal

🎧 Hallgasd a cikket: Lejátszás Szünet Folytatás Leállítás Nyelv: Auto…

Read more >

{kind=link}