Performing on the parallel bars, in the spirit of Porter

The Business Days in Tapolca were great, my presentation was also good, but afterwards I was thinking more about what I had missed from my presentation than usual. I would have never thought that the new ‘regulation’ of retail will be an even bigger motivation for writing than the reasons for writing the ‘Retro’ series. First and foremost I would like to make it clear that I know what it feels like to negotiate from a position where the number of competitors is high and some of them cut corners. My suggestion for everyone is to look in the mirror – if you do this long enough, with honesty and the necessary professional knowledge you have already taken the first step on the right path. My presentation in Tapolca made an attempt to give an entertaining recipe for this. To add a few more things to my presentation, let us rely on the help of Michael Porter. The negotiating position of suppliers is determined by the famous ‘five forces’ tables. From suppliers’ point of view it is most important to understand the characteristics of barriers to entry. This is the decisive factor in competition and in suppliers’ bargaining position. Very few suppliers can cover themselves with substitute products too. Those who would like to limit these conditions are acting against the freedom of retail and the market. In the case of Hungary artificial protection makes companies lazy and when the transitional period is over, ‘protected’ companies will be the first to go bankrupt. As for economies of scale: it is a serious limitation that can keep both discounts and background conditions below 10 percent. Usually it is characteristic of primary processing industry (sugar, flour, cooking oil). Market leaders are not domestic but regional players.10/10% was indicated on the slide in my presentation. Differentiation: the favourite competitive advantage of brand builders. Advantages here are very volatile and those who are able to differentiate themselves steadily are the fixed stars on the sky of brands, while the rest are simply comets. 5-20%/5-20% was seen on the presentation slide. Simple capital strength can lead to success and is featured in the model only as a capability when a fierce price competition is forced upon competitors; the presentation number was 30%/0. The fourth barrier: limitations posed by the learning curve and production costs. Champions of production costs are often strong private label manufacturers as well. In this category the numbers are 0-5%/ 5-10%. Access to distribution channels: I am in favour of proportionate and realistic listing and keeping-on-the-list fees. Listing exists because space on store shelves is limited – a product that used to be there is taken off in favour of one that has not proven yet. Keeping a product on the list is used to keep away new contestants. My sample number here is 5-20%/5-20%. If we add up all the numbers the end result is more than 100 %. Therefore it is worth reading Michael Porter’s analyses in knowledge of the above framework numbers and think about the position of our companies in this system of relations.

Related news

Related news

OKSZ: Household consumption cannot keep up with the growth rate of real wages

🎧 Hallgasd a cikket: Lejátszás Szünet Folytatás Leállítás Nyelv: Auto…

Read more >

KSH: retail turnover in February exceeded the same period of the previous year by 3.8 percent and the previous month by 0.4 percent

🎧 Hallgasd a cikket: Lejátszás Szünet Folytatás Leállítás Nyelv: Auto…

Read more >

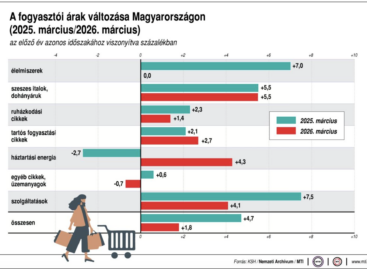

In March, consumer prices exceeded the values of the same month of the previous year by an average of 1.8 percent

🎧 Hallgasd a cikket: Lejátszás Szünet Folytatás Leállítás Nyelv: Auto…

Read more >

{kind=link}