Favorable mid-year changes in the taxation of primary agricultural producers

From July 15, 2023, the primary agricultural producer may, in addition to certified costs and depreciation, reduce the income from the sale of the equipment used for his activities by the investment costs of the purchased tangible assets, under certain conditions.

(Photo: Pixabay)

The favorable rules also apply to assets sold after January 1, 2022. As of January 1, 2022, the sale of business equipment used for primary production activities, such as the utilization of a tractor or a barn, is not considered an additional primary production activity,

- the income from this should therefore not be taken into account among primary producer income,

- the income and the tax payable must be calculated according to the rules for income from the transfer of movable or immovable property.

According to the new rules, primary producers can deduct depreciation from the income from the sale of tangible assets used for their activities, which are used exclusively for business purposes, as well as certified costs, i.e. the amount spent on acquisition and value-enhancing investments, if they have not yet been offset against their income from primary producer activities. accounted for as an expense. The income received from the sale of these assets can be further reduced by the investment cost of tangible assets used for the primary producer’s activity, which serve only operational purposes, and which the primary producer has not yet accounted for as depreciation. The condition for this is that the primary producer acquires the latter tangible assets in the current year or the year following the current year until the tax return is submitted, but no later than the return deadline. The primary producer must record in the register of fixed assets, which fixed asset’s investment cost reduces the income from the sale of the fixed asset.

The part of the investment cost that exceeds the income from the transfer can be accounted for by the primary producer as depreciation

The primary producer can also reduce the income from the sale of tangible assets sold after January 1, 2022 by the investment cost of the purchased tangible assets. Thus, the tax paid on the income from the transfer of movable property shown in the 22SZJA return due to the sale of tangible assets sold exclusively for business purposes in 2022 can be reclaimed by self-auditing the return.

National Tax and Customs

Related news

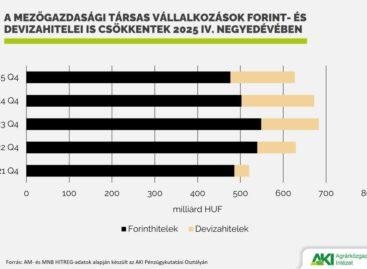

Agricultural loan portfolio decreased in 2025

🎧 Hallgasd a cikket: Lejátszás Szünet Folytatás Leállítás Nyelv: Auto…

Read more >

At the initiative of Hungary, another EU source will help farmers affected by last year’s drought

🎧 Hallgasd a cikket: Lejátszás Szünet Folytatás Leállítás Nyelv: Auto…

Read more >

Strengthening the pig sector continues with support for breeding sow farmers

🎧 Hallgasd a cikket: Lejátszás Szünet Folytatás Leállítás Nyelv: Auto…

Read more >Related news

Oat-based “feta” wins the cheese innovation competition of Lidl Germany and ProVeg

🎧 Hallgasd a cikket: Lejátszás Szünet Folytatás Leállítás Nyelv: Auto…

Read more >

Finger Food Experience

🎧 Hallgasd a cikket: Lejátszás Szünet Folytatás Leállítás Nyelv: Auto…

Read more >

KPMG: Easter boom: the season is exploding for families, retail and the chocolate industry

🎧 Hallgasd a cikket: Lejátszás Szünet Folytatás Leállítás Nyelv: Auto…

Read more >

{kind=link}